What Is Gap Insurance?

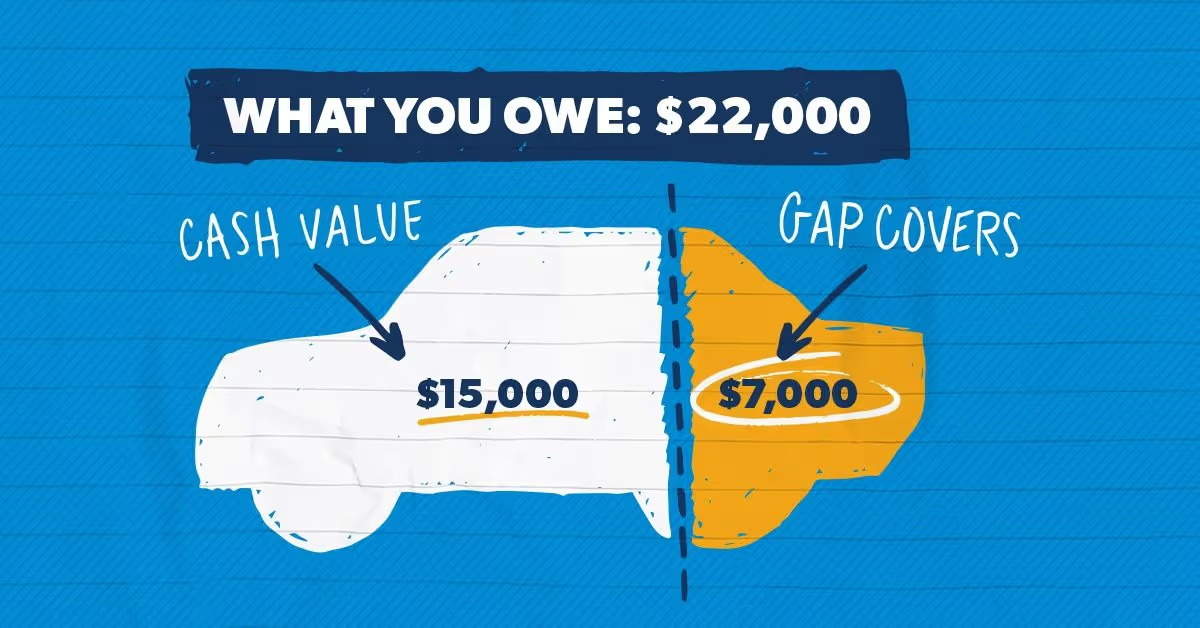

Gap insurance covers the difference between what you owe on your car lease and what the vehicle is actually worth if it gets totaled or stolen. Without it, you could owe thousands out of pocket on a car you can no longer drive.

How Much Does Gap Insurance Cost?

The cost depends entirely on where you buy it. Here is what you should expect in 2026:

Dealer Gap Insurance

Dealers typically charge $500 to $1,000 as a lump sum rolled into your leasing. That sounds manageable until you realize you are paying interest on it for the life of your lease. On a 60-month loan at 6% APR, a $700 gap policy actually costs you $812.

Insurance Company Gap Coverage

Your auto insurer may offer gap as an add-on for $3 to $15 per month depending on your vehicle and coverage level. This is almost always cheaper than the dealer and you can cancel anytime.

Credit Union Gap Insurance

Credit unions often include gap insurance with auto loans for $200 to $400 flat. Some include it free with certain loan products.

Standalone Gap Policies

Companies that specialize in gap coverage sell policies for $150 to $350 for the full term. No markup, no leasing charges.

When Do You Actually Need Gap Insurance?

Gap insurance makes financial sense in specific situations:

- You put less than 20% down on a new car

- Your lease term is longer than 36 months

- Your vehicle depreciates faster than average (luxury cars, certain sedans)

- You rolled negative equity from a previous loan into your current one

- You are leasing (most leases require gap coverage)

If you put 25% or more down, drive a vehicle that holds its value well, or have a short loan term, gap insurance is probably unnecessary.

Lease vs Loan: Different Gap Rules

Most lease agreements include gap coverage automatically. Check your lease contract before buying a separate policy. Paying for duplicate gap coverage is one of the most common unnecessary expenses in car leasing.

For leased vehicles, gap is almost never included. You need to add it yourself, and the sooner you do it, the better the coverage window.

How to Get the Best Price on Gap Insurance

- Never buy gap insurance from the dealer F&I office without comparing prices first

- Call your auto insurance company and ask about gap add-on pricing

- Check your credit union if you have one

- Get a standalone quote from a gap specialist

- Ask your broker. Vantage Auto Group can source gap coverage at wholesale pricing

Bottom Line

Gap insurance is a smart purchase in the right situation, but most people overpay by buying it from the dealer. The same coverage costs 50-70% less from your insurer or a standalone provider. When leasing through Vantage Auto Group, we will make sure you have the right coverage at the right price.

.avif)