Car lease contracts use a specific vocabulary that is rarely explained well at the dealership. This glossary defines the 30 most important terms you will see on a NJ lease agreement, what each one actually means, and why each one matters for your monthly payment, total cost, or end-of-lease decision.

Use it as a reference when you are reviewing a deal sheet, comparing two leases, or trying to understand a contract before signing. Each term is explained in plain English, with the math implications and any NJ-specific context where it applies.

Money Terms

Capitalized cost (cap cost)

The agreed-upon price of the vehicle for the lease, before any down payment or rebates. Roughly equivalent to the purchase price you would pay if you bought the car outright. Lower cap cost means lower monthly payments. This is the single most negotiable number in your lease.

Gross capitalized cost

The total starting price before any reductions. Includes the vehicle's sale price, taxes (where applicable), title and registration, and any add-ons like extended warranties or GAP insurance.

Adjusted capitalized cost

The gross cap cost minus any cap cost reduction (down payment, trade-in equity, or rebates). This is the actual amount used to calculate your monthly payment.

Cap cost reduction

Any payment that lowers the cap cost upfront. Down payment, trade-in value, dealer rebates, manufacturer cash incentives, and loyalty or conquest cash all qualify. Each dollar of cap cost reduction reduces your monthly payment.

Money factor

The lease equivalent of an interest rate, expressed as a small decimal like 0.00125 or 0.00250. Multiply the money factor by 2,400 to get the rough APR equivalent (so 0.00125 equals 3.0 percent APR). Lower money factor means lower monthly payments. (See our full guide on money factor.)

Residual value

The leasing company's prediction of what the vehicle will be worth at lease end, expressed as a percentage of MSRP. Higher residual value means lower monthly payments because you are only paying for the depreciation between the cap cost and the residual. A 36-month lease on a vehicle with 65 percent residual will have a meaningfully lower payment than the same vehicle with 50 percent residual. (See our full guide on residual value.)

Buyout price (purchase option price)

The pre-set price at which you can buy the vehicle at lease end. Calculated when you sign the lease. The price is locked in your contract and does not change based on the actual market value at lease end. When residual values are set conservatively (lower than actual end-of-lease market value), the buyout price can be a good deal. (See our guide on lease buyout decisions.)

MSRP (Manufacturer's Suggested Retail Price)

The sticker price the manufacturer recommends. The cap cost in your lease should usually be lower than MSRP, often meaningfully so depending on dealer competition. MSRP is a reference point, not a price you should accept.

Invoice price

What the dealer paid the manufacturer for the vehicle, before holdback and incentives. Many dealer payment programs are tied to invoice price, so it is sometimes used as a reference point in pricing. The invoice price is usually 5 to 10 percent below MSRP.

Acquisition fee (bank fee)

A one-time fee charged by the leasing company to set up the lease. Usually $595 to $895 depending on the brand. It is non-negotiable in most cases but can sometimes be rolled into the cap cost rather than paid upfront.

Disposition fee

A one-time fee charged at lease end if you return the vehicle (vs buying it out or transferring it). Usually $300 to $500. The fee covers the leasing company's cost to inspect, clean, and resell the returned vehicle.

Time and Mileage Terms

Lease term

The length of the lease, almost always expressed in months. The most common terms in NJ are 24, 36, 39, and 48 months. Longer terms have lower monthly payments but expose you to more depreciation and warranty issues. 36 months is the most common balance point.

Mileage allowance

The total miles you are permitted to drive over the term, before excess mileage charges kick in. Common allowances are 7,500, 10,000, 12,000, and 15,000 miles per year. Higher mileage allowances increase the monthly payment because the leasing company has to lower the residual value to account for the additional wear.

Excess mileage charge

The per-mile fee charged if you drive over your mileage allowance during the lease. Usually $0.15 to $0.30 per mile, listed in your contract. If you have exceeded the allowance, you pay this fee at lease end. (See our guide on going over mileage on a lease.)

Low-mileage lease

A lease structured for drivers who do less than 10,000 miles per year. The lower mileage allowance produces a lower monthly payment, but exceeding it triggers excess mileage charges. Best for retirees, hybrid commuters, or households with multiple vehicles.

High-mileage lease

A lease structured for drivers who do 15,000 to 25,000 miles per year. The higher mileage allowance increases the monthly payment but matches typical drivers who would otherwise face large excess mileage charges. Best for sales reps, ride-share drivers, and long-distance commuters.

Cost-at-Signing Terms

Down payment (money down)

Cash you pay upfront to reduce the cap cost or roll into the deal. Down payment is technically optional on a lease, but most lease deals quote a down payment to keep the advertised monthly payment low. Higher down payment means lower payment, but if the car is totaled in the first 6 months, you may lose your down payment. Many NJ lease shoppers ask about $0-down lease options for this reason.

Drive-off cost

The total amount paid at lease signing. Typically includes first month payment, taxes, registration, acquisition fee, and any down payment. Sometimes called out-the-door or due at signing. A $0-down lease still has a drive-off cost (usually under $1,000), because first month's payment and acquisition fee still apply.

Due at signing

Same as drive-off cost. The dollar amount you bring to closing. Lease deals advertised as due at signing should be compared apples-to-apples (some hide larger acquisition fees in this number).

Security deposit

A refundable deposit, typically equal to one or two months' payment, held by the leasing company against any end-of-lease charges. Most major manufacturers eliminated security deposits years ago. If a leasing company is asking for one in 2026, ask why.

First month's payment

Always due at signing as part of the drive-off cost. Lease payments are paid in advance: the first month's payment is for the first month of the lease, paid at signing. Subsequent payments are due monthly.

Ending the Lease Terms

Lease return

The end-of-lease process of returning the vehicle to the leasing company. Includes a final inspection, mileage reconciliation, and any wear and tear charges. Most leasing companies allow lease return up to 30 days before or after the contract end date. The Federal Reserve's end-of-closed-end-lease guide walks through every charge that can apply at lease end.

Buyout option (purchase option)

The contractual right to purchase the vehicle at lease end at the pre-set buyout price. Not a requirement. The lease terms include a window (often 30 to 60 days before lease end) when you must declare your intent to buy.

Wear and tear

Normal cosmetic and mechanical wear that the leasing company expects after the term of use. Each leasing company has its own wear-and-tear standard. Generally, light scuffs, minor scratches, and tire wear within spec are normal. (See our full guide on excess wear and tear charges.)

Excess wear charges

Charges for wear that exceeds the leasing company's normal wear-and-tear threshold. Common examples: dent larger than 2 inches, paint damage exposing primer or metal, tire tread below 4/32 inch, missing or damaged interior trim. Charges range from $50 to $1,500 depending on damage severity.

Lease transfer (lease assumption)

The process of transferring your lease to another person, who takes over the remaining payments and assumes responsibility. Allowed by most major leasing companies but with restrictions and a transfer fee ($300 to $600). Sites like Swapalease and LeaseTrader connect transferors and transferees. (See our complete guide on how lease transfers work.)

Documentation and Legal Terms

Lease agreement (lease contract)

The legal contract between you and the leasing company, signed at the dealership. The document is dense but every important number should be visible: cap cost, money factor, residual, mileage allowance, total payments. Read it before you sign. NJ MVC requires specific disclosures on every lease contract.

Lessor

The company that owns the vehicle and is leasing it to you. Almost always the manufacturer's captive finance arm (Toyota Financial Services, BMW Financial Services, Ford Credit) or a major leasing company.

Lessee

The person leasing the vehicle. You.

Closed-end lease

The standard consumer lease. The buyout price is locked when you sign and does not change. You can return the vehicle at lease end with no further obligation beyond mileage and wear charges. This is what almost every NJ consumer lease is.

Open-end lease

A lease where the buyout price floats based on the market value at lease end. If the vehicle is worth less than expected, you owe the difference. Almost exclusively used for commercial fleets, not consumer leases. If a NJ broker or dealer offers you an open-end lease for personal use, walk away.

Lien holder

The leasing company holds the title to the vehicle during the lease term. They are the lien holder. You are the registered driver and have title only after you exercise a buyout option and pay the buyout price.

NJ-Specific Lease Terms

NJ sales tax on leases

NJ charges sales tax on the monthly lease payment, not on the full vehicle price. This makes NJ lease tax handling simpler than some other states. Trade-in value reduces the taxable amount, which is why trading in through a broker (or via Vantage Motor Car for the used side) can save sales tax in addition to direct cap cost reduction. Full NJ rules are documented in the state's Consumer Automotive Tax Guide from the NJ Department of the Treasury.

NJ MVC title transfer at lease end

If you choose to buy out the vehicle at lease end, the title transfer goes through the NJ MVC. The leasing company releases the lien and signs the title over. You file for new registration and pay the buyout price plus title transfer and registration fees.

NJ vehicle inspection

NJ requires a state inspection on every leased vehicle, valid for 2 years on cars 5 years old or newer. The first inspection is usually included in your dealership delivery. After that, it is your responsibility through the NJ MVC.

NJ documentation fee (doc fee)

Charged by the dealership at signing, covers the dealership's administrative work on the deal. NJ does not cap doc fees, so they vary widely (from $89 at some dealerships to $700+ at others). Always ask why and try to limit this charge during negotiation.

Common Acronyms

APR (Annual Percentage Rate)

The interest rate equivalent on your lease, derived from the money factor by multiplying by 2,400. APR is the easier number to compare across lease vs finance options.

MF

Shorthand for money factor in lease quotes and online discussions.

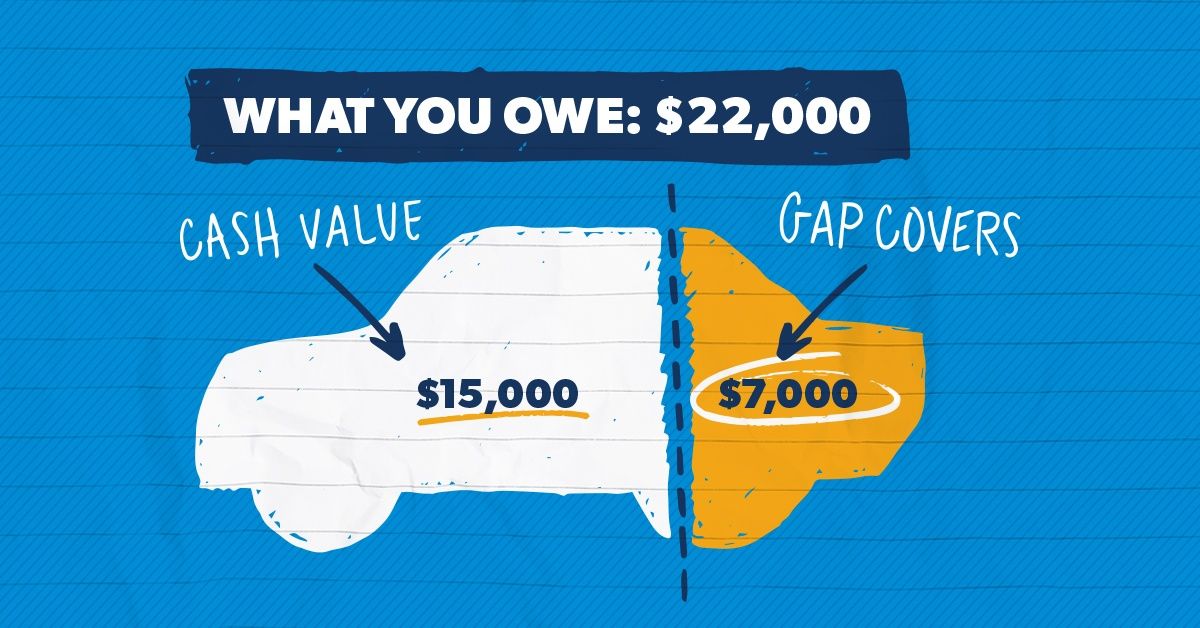

GAP (Guaranteed Asset Protection)

Insurance that pays the difference between your insurance settlement and the buyout price if the vehicle is totaled. Usually included in NJ lease deals at no extra cost, but always verify in your contract. Without GAP, a totaled lease could leave you owing the leasing company several thousand dollars.

OEM (Original Equipment Manufacturer)

The vehicle manufacturer (Toyota, Honda, Ford). Used to distinguish OEM-installed accessories from aftermarket additions, especially relevant for warranty and lease return.

CPO (Certified Pre-Owned)

A used vehicle that has passed a manufacturer-backed inspection and carries a warranty similar to a new vehicle. CPO leases (when available) offer lower monthly payments than new while preserving most of the warranty protection. Vantage Motor Car handles CPO sourcing and sales as a separate operation from the new-car broker model.

Putting It All Together

The math of any lease deal comes down to a few key numbers that connect through the formulas above. The monthly payment is roughly: (cap cost minus residual value) divided by lease term, plus (cap cost plus residual value) times money factor. Lower cap cost, higher residual, lower money factor: lower monthly payment.

When you compare two NJ lease deals, the apples-to-apples comparison is the total cost of the lease over the full term, including drive-off cost, all monthly payments, expected mileage charges, and any anticipated end-of-lease fees. Two leases with the same advertised monthly payment can have meaningfully different total costs depending on these other line items.

When evaluating any lease, ask for the breakdown of: gross capitalized cost, cap cost reduction (and what is included), adjusted capitalized cost, money factor, residual value, mileage allowance, and term length. With those seven numbers, any car shopper can independently calculate the monthly payment and verify it against what is advertised.

Further Reading and Authoritative Sources

The State of New Jersey's Division of Consumer Affairs publishes a comprehensive auto leasing guide that covers NJ-specific consumer protections and disclosure rules: Guide to Auto Leasing (NJ DCA).

For federal-level consumer protection and the underlying laws governing how leases are structured and disclosed, the Federal Reserve maintains a complete resource at End of Closed-End Lease (Federal Reserve), and the Consumer Financial Protection Bureau covers the lease vs buy decision at CFPB Leasing vs Buying a Car.

Bottom Line

A lease is a long-term financial agreement, not a price tag. Understanding the vocabulary above means walking into the dealership knowing what each line item actually represents and which numbers are negotiable.

If you are evaluating a NJ lease and want a second pair of eyes on the numbers, or if you would prefer to skip the dealership process entirely, Submit a Quick Quote and Vantage will source competitive pricing from dealer partners on your specific make and model. Vantage explains every line item on every quote in plain English, with the underlying numbers visible and the broker fee disclosed in writing before any work begins. (For more on broker fees, see how much does a car broker cost.)